I kid, of course. The market is up 200 points today, not because GM is filing bankruptcy, but rather because investors seem to understand that the event itself is not at all catastrophic. After all, Chrysler is emerging from bankruptcy shortly and actually saw sales go up after they filed. It seems that most people, investors and car buyers alike, understand that Chapter 11 is a legal corporate process first and foremost and should be an afterthought to car buyers. Still, who would have thought the market would react quite so well initially?

Two short points on GM. First, the stock is up 20% today to about 90 cents. It's worthless, folks. Those who still grip their "efficient markets hypothesis" tightly can use this as a perfect case study against the theory.

Second, how will we be able to judge whether "New GM" is viable long term after they emerge from bankruptcy (which many say will be before summer ends)? It's all about cost structure. Many attribute their latest woes chiefly to the weak economy and lack of credit, but they seem to have forgotten that GM was a money loser in 2006 and 2007, when credit was flowing more freely than any other time in our history.

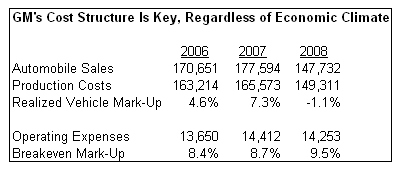

Consider the chart below, which shows how far from profits GM has been over the last three years:

As you can see, GM needed a near-10% mark-up over cost to breakeven on their vehicles. They never hit that goal in 2006-2007, even before they started selling cars for less than they built them for in 2008. If "New GM" can get their costs down, and have them be predictable and stay low, the company might be able to make a comeback down the road. It won't be easy, but Chapter 11 was the only way to make it even a reasonable possibility.

Full Disclosure: No position in GM, past or present.