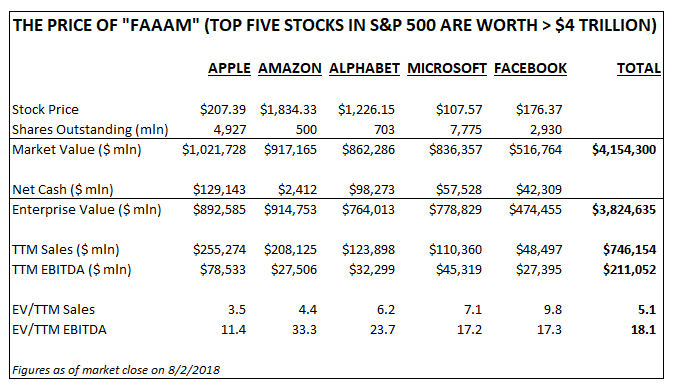

Mega cap technology companies are now facing heat as the federal government continues the process of investigating their market positions as it relates to antitrust/monopolistic issues. Some politicians are calling for breakups of tech companies. The narrative within the investing community seems to be that Microsoft (MSFT) was severely crippled by an antitrust settlement nearly 20 years ago, and as a result, this could get ugly for today's tech leaders as the FTC and DOJ take closer looks.

So I decided to go back and see exactly how stifled Microsoft's growth was after the government's lawsuit was settled in 2001. The answer might be surprising:

MSFT Fiscal 2001 Sales: $25.3 billion

MSFT Fiscal 2001 EBITDA: $13.2 billion

MSFT Fiscal 2011 Sales: $69.9 billion (+176% vs decade prior)

MSFT Fiscal 2011 EBITDA: $29.9 billion (+126% vs decade prior)

If the Microsoft case is supposed to be the poster child for how a government lawsuit can kill your business, it does not seem to be much of an issue, and certainly not to the extent investors are worried right now. Interestingly, while MSFT initially lost their case, they prevailed nicely during the appeals process, which ultimately led to a settlement that had the effect of "limiting" the company's EBITDA growth rate to +8.5% annually for the ensuing 10-year period, with revenue rising even faster (+10.7% annually).

Keep in mind that we are very early on in the process today, with regulators just now deciding who will take a look at each company. It will take years for them to draw a conclusion, possibly file a lawsuit, potentially prevail in court, then have to defend during an appeal even if they win, and only then would tech firms have to adapt to any stipulations.

Perhaps more importantly, I think it is helpful for us, as users of these tech products, to ask ourselves if we believe that the mega tech companies of today have grown so large because they have created things that consumers find helpful and value-creating in their lives, or if it is more due to them simply using their power to force consumers to use their stuff. Perhaps more now than at any other time, it seems to me to be the former. As a result, it is hard to argue that consumer are being unfairly harmed with offerings such as free 1-2 day shipping with Prime, a free multi-featured Google Maps app for their phone, and a social network platform where anyone can sign up, post anything they want, and share it with whomever they want.