Economic bubbles are inevitable, much like the business cycle, but history shows they oftentimes don’t repeat in exactly the same way. For instance, I don’t think it’s likely we see another real estate bubble inflated by interest-only, pick-your-payment, or no-doc income loans, but there are other ways for property values to go bonkers. I would have said the same thing about the late 1990’s dot-com bubble, and I would have been wrong.

Those of us who remember that time period recall that profitless companies with little more than a lackluster business model saw share prices surge just by issuing an “internet-related” press release. We were told the market opportunity was so big that the current iteration of the product or service didn’t matter, let alone the valuation of the company. Businesses with real revenue were losing money but since the market opportunity was so large, we could try and justify paying 20 times sales instead of 20 times earnings. The big cap stocks back then played out a little differently, with stocks like Cisco and JDS Uniphase fetching more than 100 times earnings (compared with 25-40 times for Apple, Microsoft, and Google this cycle).

The rise and subsequent fall of Ark Invest’s flagship Innovation ETF (ARKK), special purpose acquisition companies (SPACs) targeting story stocks with a path to revenue five years out, and another general IPO boom (why is Allbirds public?) have largely mirrored the environment from 20+ years ago. We have fancy new terms (large market opportunity replaced with “TAM,” dot-com replaced with “innovation”) but the end result was nearly identical; profitless companies trading for insane valuations based on a dream of every good story becoming the next Amazon.

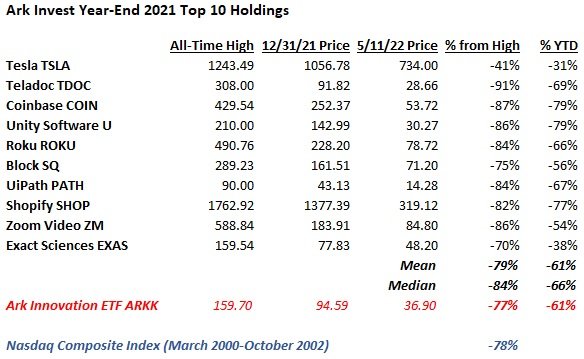

Exactly how close have we come to those olden days? Well, from the March 2000 peak (5,132) to the bottom in October 2002 (1,108), the Nasdaq Composite index fell by 78%. Take a look at the average decline for Ark Invest’s top 10 holdings (as of year-end 2021) from their peak:

Talk about deja vu.

Will the Nasdaq fall 78% again this time around? I doubt it because the biggest constituents today include many of the aforementioned names that are richly valued but never got to bubble territory. They alone should prop up the index in relative terms. As of today the Nasdaq is down 30% from the November 2021 peak. I think it’s more likely than not that the index doesn’t even get to minus 50% because of the mega caps.

Regardless, should we be worried? Well, no doubt the short term pain has been brutal. Although I didn’t chase the “innovation” highfliers shown above, I have been adding to my tech exposure as prices drop and have lots of red ink to show for it now. But I think the longer term outlook is pretty darn good for the highest quality businesses.

Why? Well, we are starting to see certain companies begin to acknowledge that the bubble is over and pivot towards cutting back on hiring and overall spending in order to turn operating losses into profits. They realize that showing revenue growth is not going to work for Wall Street anymore so margins have likely troughed for this cycle. The Uber CEO was recently very explicit that this is the route they are now taking and while the stock hasn’t reacted yet, I think they will prove to be a long-term winner and quite profitable over the intermediate term.

Not every company will go this route right away and they will find it hard to raise more money to keep the cycle going. They missed the chance to raise $5 billion at a $50 billion valuation - 10% dilution looks paltry now - and they will get an earful if they try to raise the same amount with a $10 billion valuation. But give it 6 or 12 months and I think most will come around to the idea that even innovative companies need to breakeven or make a little money.

I also expect the new environment will accelerate M&A activity. Bigger firms can bulk up and take out one of the many new competitors (do we really need so many SAAS companies or EV manufacturers?) and the cost synergies that come with a deal will also accelerate the margin expansion that investors now crave. I would not have guessed that Twitter would be the first big deal to get announced (and it’s a bit of a unique circumstance), but more deals should follow after everyone catches their breadth and the public markets stabilize a bit.

As for how I am approaching the current environment, I am fairly unconcerned if shares move against me right away (I’m not going to catch the bottom - I just want my cost basis to look solid 2-3 years from now). Many stock prices will look silly in the near-term if you believe they will emerge as leaders (Uber at half the IPO price despite the company having doubled revenue since then and having committed now to moving towards profitability?) but I am focused on trying to buy the winners cheaply regardless of what the next 3-6 months bring.

The current market reminds me of the Warren Buffett line that he wouldn’t care if the market closed for a few years. If you see a company you like for the long-term and the valuation finally looks compelling, I can’t help but suggest that maybe you buy it and put it away for 3-5 years rather than try and make sense of the near-term outlook and/or dynamics.

Full Disclosure: Long UBER at the time of writing but positions may change at any time