With the stock market rallying in recent weeks over optimism for a relatively smooth nationwide reopening of the economy, and daily trading becoming a little more calm (day traders speculating in bankrupt equities notwithstanding), I am able to take a breath now that earnings season is mostly over and reflect on the past few months. Of course, a second wave of virus could quickly bring back volatility and fear, but let’s stay positive.

The tables have turned pretty quickly and I am now actually finding opportunities to lighten up on securities that I was buying during the height of the recent market meltdown. As was the case when I was bargain hunting with fresh client cash in March, I am trying to keep things simple.

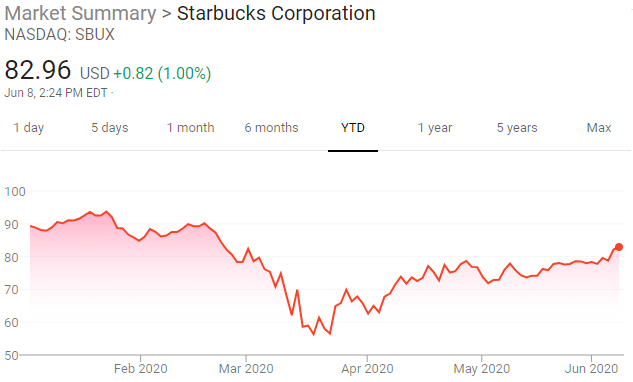

Take a stock like Starbucks (SBUX). Great business. Blue chip stock that typically fetches a premium (and deservedly so). Today it trades 8% below its February 19th (market peak) level. Seems about right to me, as their business is likely not permanently impaired at all by the pandemic, but sales volumes and margins will take time to rebound to pre-covid levels. At its worst point SBUX was 45% below its $90 pre-covid print, which was most certainly irrational given that about half of their locations remained open during the stay-at-home orders. Buying SBUX in the 50’s was obvious and came with minimal risk. Paring it back in the 80’s seems obvious too.

It can be easy to get stuck in the weeds during massive market drops, but when most securities are on sale, it is best to stick with the simplest stories. Take a company like Bright Horizons (BFAM), a leading daycare provider. Sure it is financially stressing for the company when the bulk of its centers are closed, but the bearish thesis for BFAM over anything but the short term seemed odd at best and downright silly at worst; post-pandemic everybody is going to work from home, care for their children in the next room, and maintain the same level of productivity and/or sanity? I don’t think so. And yet BFAM shares sank from $175 on February 19th to the mid 60’s in March. Down by two-thirds for a leading daycare company with a strong balance sheet? These are easy and simple bets to make if we look out 6 months or a year.

One last example is Vereit (VER) a commercial landlord for single tenant buildings. While tenants like drugstores and dollar stores kept paying, VER still only received 75-80% of contractual rent payments for April and May. Should the stock have fallen on that? Of course. But how much should a REIT fall if they are collecting the bulk of rent and are still fully covering operating expenses and debt service? In this case, investors felt that 65% was the right number, as the stock fell from $10.00 to $3.50 per share at its low point. In fact, the entire real estate universe fell by 50-80% regardless of actual rent collections.

In each of these examples, the simplicity of the story should have given investors a sense of confidence when allocating capital into falling markets. The leading global coffee retailer is a survivor. Parents will keep sending their kids to daycare post-pandemic. A landlord collecting 75% of rent should not see its stock trade down by 65%.

Now, this is all easy to say and harder to do. Did I also find myself delving into more complex and riskier bets, rather than putting all of my capital into BFAM, SBUX, and VER? Yes. Consider taking the plunge into an airline, cruise operator, or hotel company and ask if the undervalued nature of the stock was as easy to see (and pinpoint to an exact figure). It is rare to be able to maintain such focus and discipline and only target the most obvious buys in a sea of bargains. But as value investors when we look back and grade ourselves a year after a bear market, it is usually the case that the simplest stories brought with them the best risk-adjusted returns.

Full Disclosure: Long BFAM, SBUX, and VER (as well as CCL, LUV, and PEB) at the time of writing, but positions may change at any time