We see this happen so many times. A hot brand new technology hardware company with a cool new product decides to cash in via an IPO. All is good for a little while and then Wall Street's expectations for growth become too ambitious as competition grows and the need to constant upgrade one's device wanes. The company misses financial targets for a few quarters in a row and the stock goes from darling to laughingstock in short order. I think we can all agree that fitness band maker Fitbit (FIT) fits the bill. Here is the stock's chart since the IPO in mid 2015:

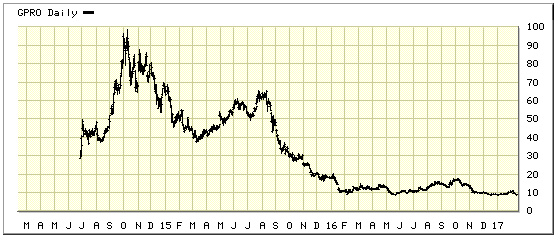

Another obvious poster child for this phenomenon is GoPro (GPRO):

To me, it seems the only logical play is for these companies to be acquired by larger technology companies who can best harness the value and loyalty behind these solid brands to maximize their profit potential.

So why should a bigger tech player swoop in and take Fitbit and GoPro out of their misery? Quite simply, the public markets become broken for these young disappointments very quickly. Given the competitive landscape, it will be very hard for either of them to reaccelerate its business to the level that would be required for investors to warm back up to the story. As a result, the stocks are being valued extremely cheaply if you consider the value of the brand and the current user base. As a result, it should be a no-brainer for the big guys to snap up the small fries. This becomes especially true if we consider that the IPO markets have allowed these smaller players to amass large cash hoards.

Take Fitbit, for instance. At less than $6 per share, FIT current equity value is a meager $1.4 billion. The company's finances are actually is very solid shape, with no debt and a projected $700 million of cash onhand as of year-end 2016. Net of cash, Wall Street is valuing the Fitbit brand and the more than $2 billion annual revenue base (2016 figure) that it brings are just $700 million. For a strategic acquirer, that price should be mouth-watering. Even offering a big premium of 50-100% to persuade current shareholders to sell would not impede value-creation from the deal. Offer $11 per share/$2.7 billion for FIT ($2 billion for the operating business plus cash onhand) and it is unlikely a company like Apple or Google would regret it.

GoPro would be an even cheaper purchase. At the current $8.75 share price, Wall Street thinks the company is worth just $1 billion (net of $200 million cash, no debt). Could Apple not add value to its company by paying $2 billion for GoPro, innovating the product line further, and integrating it into their existing user base around the globe?

So why have these deals not really happened? In some cases, large tech companies firmly believe they are superior to the upstarts. As a result, they prefer to challenge them with internal product development (me-too copycats) instead of merging and taking out one of their competitors. Apple is probably the most prominent company in this category, as they refuse to acquire any meaningful competitor. And yet, it is almost assured that their competitive positions would be stronger today has they bought companies like Netflix, Spotify, Pandora, etc. Instead, we read stories like the one recently that said that Apple is planning to go into the original content business. All I can do is roll my eyes.

The second hurdle for these combinations is seller willingness to merge. From an emotional perspective, the board of GoPro would not have an easy time agreeing to sell the company for $15 or $20 when the stock price was $100 in 2014 and $60 in 2015. If they just come out with one more hit product the sky could be the limit! Same thing with Fitbit; we went public at $20 in 2015, how can we sell out for $10?

To me the playbook is obvious. Wall Street is telling you that your hyper growth days are over. The big guys have more resources and will slowly take your customers. For some reason, nobody realizes that combining forces is probably the best move for both sides in the long run. I will be interested to see if Fitbit and GoPro are public companies a year from now. Heck, maybe Steve Ballmer comes back to Microsoft and sees synergies with a Nokia/Surface/Fitbit/GoPro/X-Box product lineup (kidding, of course).